》View SMM Aluminum Product Prices, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

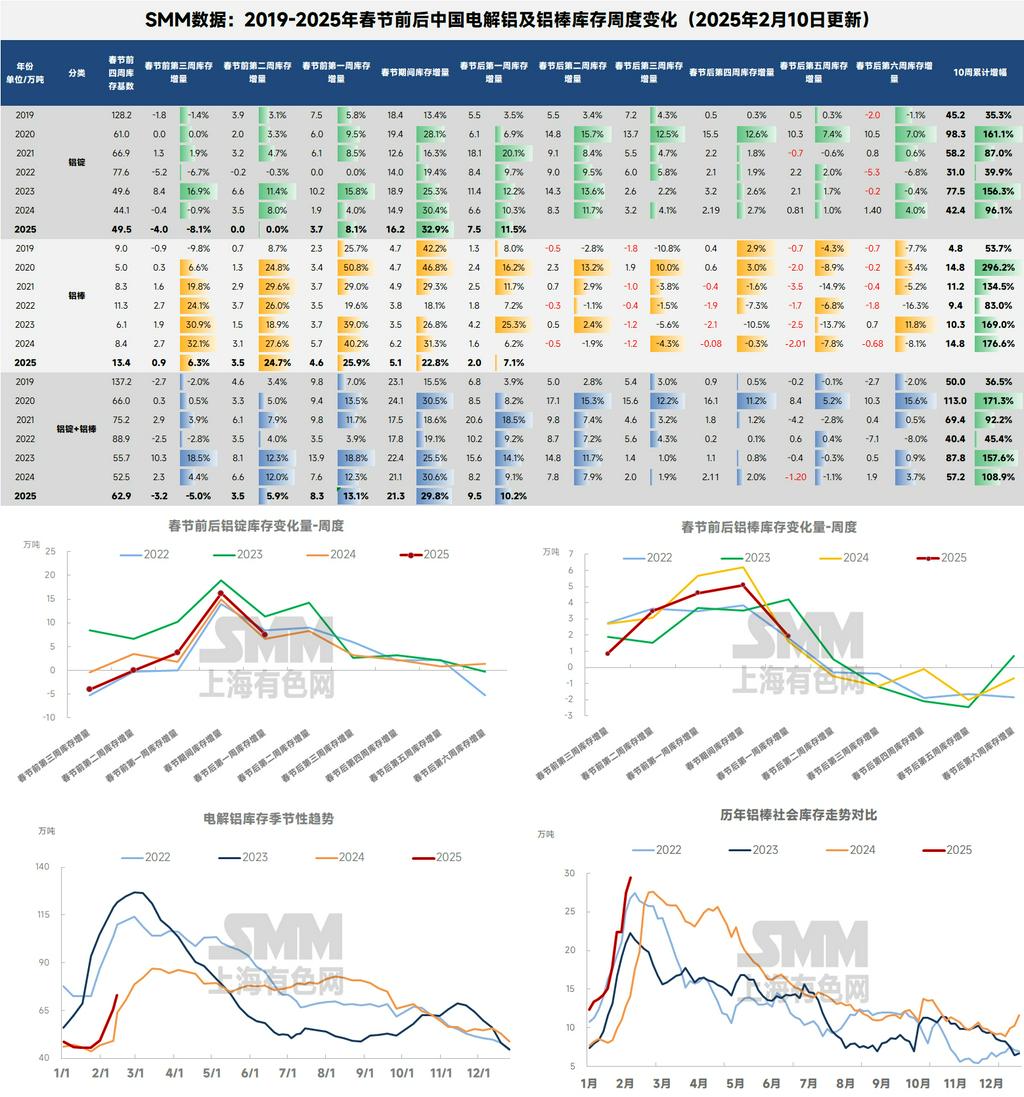

As the Lantern Festival approaches, the joy of the New Year fills the air. Most traders in the aluminum industry have resumed work this week, and downstream enterprises are expected to reach a peak in resumption of work and production soon. Let’s take a look at the aluminum inventory performance in the first week after the Chinese New Year:According to SMM statistics, as of February 10, 2025, the total domestic aluminum inventory (aluminum ingots + aluminum billets) tracked by SMM reached 1.0235 million mt, surpassing the 1 million mt mark. This represents an increase of 95,000 mt (10.2%) compared to the first day after the holiday (February 5) and an increase of 308,000 mt compared to pre-holiday levels (January 27).On a YoY basis, the inventory increase in the first week after the Chinese New Year exceeded last year’s increase of 82,000 mt and growth rate of 9.1%. The inventory buildup in the first week after the holiday continued the slightly higher trend observed during the Chinese New Year holiday.

Regarding aluminum ingot inventory, according to SMM statistics,as of February 10, 2025, domestic social inventory of aluminum ingots tracked by SMM stood at 729,000 mt, while circulating aluminum inventory was 603,000 mt. This represents an increase of 75,000 mt (11.5%) compared to the first day after the holiday (February 5) and an increase of 237,000 mt compared to pre-holiday levels (January 27).On a YoY basis, the inventory increase in the first week after the Chinese New Year exceeded last year’s increase of 66,000 mt and growth rate of 10.3%. The inventory buildup in the first week after the holiday also continued the slightly higher trend observed during the Chinese New Year holiday. Regarding outflows from warehouses, aluminum billet outflows during the holiday period (January 27-February 9) totaled 70,500 mt, which was higher than the same period last year.

By region, east China became the main contributor to inventory buildup during the holiday, primarily due to a smaller Guangdong-Shanghai price spread before the holiday and a higher Henan-Shanghai price spread compared to the same period last year. As a result, east China became the preferred destination for supplies from Xinjiang and other northern regions. During the holiday, Wuxi’s inventory increased by 85,000 mt to 258,000 mt, compared to an increase of 70,000 mt to 189,000 mt in the same period last year. Gongyi’s inventory increased by 39,000 mt to 91,000 mt, compared to an increase of 38,000 mt to 114,000 mt last year. Foshan’s inventory increased by 32,000 mt to 172,000 mt, compared to an increase of 28,000 mt to 177,000 mt last year. According to the SMM survey, due to various discount policies offered by some aluminum smelters to aluminum billet enterprises and other downstream processing plants during the holiday, the production cuts in downstream alloy plants in south China were less significant than in north China. Foshan’s inventory buildup remained slightly higher than the same period last year, mainly due to differences in supply from Yunnan compared to the same period in previous years.

Meanwhile, according to the SMM survey, Gongyi experienced concentrated arrivals during the Chinese New Year, primarily from north-west China, including Xinjiang. During the holiday, major aluminum smelting regions supplying Gongyi (e.g., Xinjiang, Qinghai, Inner Mongolia) saw varying degrees of production cuts or halts in downstream processing plants, leading to higher casting ingot production. Before the holiday, Gongyi’s inventory was relatively low, prompting aluminum smelters to focus on restocking Gongyi during the holiday. Actual inventory in Gongyi should be even higher, as some warehouses still have a large number of boxes piled up at stations, and inventory is expected to continue growing. However, there are also reports that post-holiday in-transit volumes to Gongyi are relatively controlled, suggesting a short-term rapid increase in inventory followed by a shorter duration of buildup.

SMM believes that February will remain a period of inventory buildup for domestic aluminum ingots. Based on current data, information, and historical trends, domestic aluminum ingot inventory is expected to increase rapidly in the first half of February as downstream enterprises remain on holiday before the Lantern Festival. In the second half of the month, as downstream operations resume post-holiday, the pace of inventory buildup is likely to slow significantly. Over the past seven years, only in 2021 did destocking occur in the fifth week after the holiday, with half of the years seeing destocking in the sixth week. Last year’s destocking point was even further delayed. SMM expects that under the anticipated “Golden March and Silver April” traditional peak season, as downstream operations gradually return to normal, the first post-holiday destocking is likely to occur in or before the sixth week after the holiday. The domestic aluminum ingot inventory turning point is expected around mid-March, with the Q1 inventory peak likely to reach 850,000-900,000 mt. SMM will continue to monitor downstream resumption and in-transit aluminum ingot conditions.

Regarding aluminum billet inventory, according to SMM statistics,as of February 10, 2025, domestic social inventory of aluminum billets tracked by SMM stood at 294,500 mt, representing an increase of 20,000 mt (7.1%) compared to the first day after the holiday (February 5) and an increase of 71,000 mt compared to pre-holiday levels (January 27).On a YoY basis, the inventory increase in the first week after the Chinese New Year exceeded last year’s increase of 16,000 mt and growth rate of 6.2%. The inventory buildup in the first week after the holiday also continued the slightly higher trend observed during the Chinese New Year holiday. Regarding outflows from warehouses, aluminum billet outflows during the holiday period (January 27-February 9) totaled 17,100 mt, which was higher than the same period last year.

By region, during the holiday, Foshan’s inventory increased by 16,600 mt to 117,000 mt, slightly higher than last year’s increase of 14,400 mt. According to the SMM survey, due to various discount policies offered by some aluminum smelters to aluminum billet enterprises and other downstream processing plants during the holiday, production cuts in aluminum billet enterprises in south China were generally less significant than in north China. In east China, Wuxi and Nanchang saw inventory increases of 10,300 mt and 11,000 mt, respectively, both lower than last year’s increases of 19,500 mt and 11,000 mt. Inventory increases in Huzhou and Changzhou were roughly the same as last year.

SMM believes that the first half of February will remain a period of inventory buildup for domestic aluminum billets. Based on current data, information, and historical trends, the inventory turning point for domestic aluminum billets generally occurs earlier than for aluminum ingots after downstream enterprises resume operations post-holiday. This trend is likely to continue this year. Over the past seven years, the inventory turning point for aluminum billets has mostly occurred in the second or third week after the holiday. SMM expects that under the anticipated “Golden March and Silver April” traditional peak season, as downstream operations gradually return to normal, the inventory turning point for domestic aluminum billets will likely occur in late February, with the Q1 inventory peak expected to reach 300,000-350,000 mt. SMM will continue to monitor downstream resumption and aluminum billet consumption.

On the demand side for aluminum billets, the overall operating rate of the domestic aluminum extrusion industry in the first week after the holiday reached 61.3%, showing a significant rebound compared to earlier periods. Among sub-sectors, the industrial extrusion segment performed particularly well, with some leading automotive extrusion enterprises shortening their holiday periods, providing strong support for this week’s operating rate. PV extrusion enterprises maintained stable operations with no new orders, mainly due to no significant rebound in downstream module production schedules. In the construction extrusion segment, leading enterprises resumed operations in an orderly manner after the holiday. The full resumption of the aluminum extrusion industry is expected after the Lantern Festival, as some small and medium-sized plants are still on holiday. SMM will continue to track post-holiday resumption and order recovery. (Note: Leading enterprise samples have been updated starting this week.)